- Home

- News and insights

- When should I start planning for retirement?

When should I start planning for retirement?

As long as you have some disposable income, you should start planning for retirement immediately. Retirement planning is essential in the UK, as we are enjoying longer retirements than ever before, primarily because we’re living longer. By the end of the 20th century men lived to an average age of 76 and women to 81, yet they retired earlier (on average aged 62). This extended retirement period has to be planned for and funded – and we each have to take personal responsibility for it. The earlier you start, the better.

In the article, our independent wealth planners offer their planning for retirement top tips.

Don’t rely on the government for your retirement planning

When you start planning for retirement, you cannot rely on your state pension, as Baroness Ros Altmann says in our article, ‘Five facts about retirement’, “You cannot rely on the State to support you in old age – it is up to you to make your own arrangements and plan carefully to ensure you can enjoy your later years in the comfort that you aspire to.”

If we are to realise our aspirations and attain our desired quality of life in later years, we simply need bigger pension pots than before. Even more importantly, we need to start planning for retirement as early as possible.

Start planning for retirement by calculating how much you think you’ll need

Clients almost always ask us when they start planning for their retirement, “Will I be able to retire when I want to? Will I run out of money? How can I guarantee the kind of retirement I want?” As no-one knows exactly how long they’re going to live or what financial challenges they may face, these are hard questions to answer. Pensions can be complex with so many considerations, including your family circumstances, pension rules and tax regulations.

Firstly, you will need to work out how much you have already saved and how much more you can afford to set aside. Then assess how much you think you will need to maintain your desired lifestyle and how long you realistically might live - and compare the two. This is an exercise that our independent financial planners often undertake with our clients when discussing their retirement plans. We can also build a personalised cash flow forecast for you looking at your current wealth along with your income and trying out different scenarios to see how they might work to fund your retirement.

If you would like to carry out your own assessment, use our quick calculator below to see if you will have enough money in retirement.

Take advantage of your workplace pension

Whether you are in employment or not, a partner or self-employed, you can contribute into a pension. Employers are legally bound to offer workers access to a workplace pension scheme, while anyone self-employed or unemployed who can’t invest in an occupational plan can pay into a personal pension, such as a SIPP (Self Invested Personal Pension) or a stakeholder policy.

Pensions are the most tax-efficient wrappers available to investors, with up to 45% income tax reclaimable on contributions. What’s more, many employers see their defined contribution workplace pension schemes as a valued and affordable benefit, so they offer generous contributions to their employees. If you’re an employee and not currently a member of your company’s pension scheme, ask your HR department for details.

For more details about how much you can contribute to your pension and for details of the annual pension allowance, read our article here.

Start saving for your retirement when you’re young

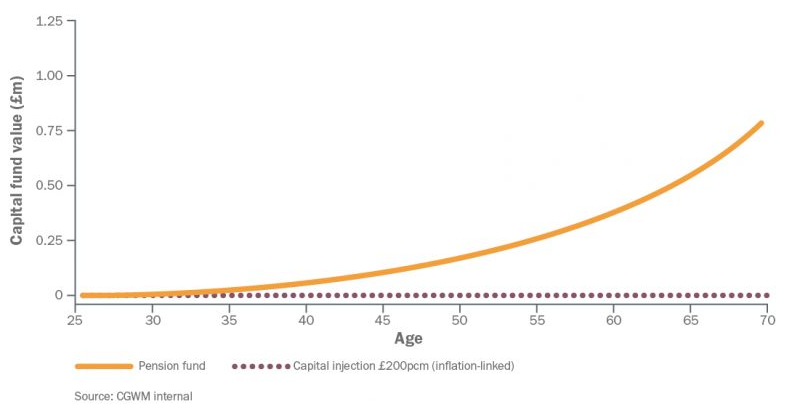

You don’t have to be a high earner to enjoy a comfortable retirement, so long as you start investing young. As the graph below shows, a 25-year-old contributing £200 each month (including employer contribution) can generate a healthy pension to supplement their state pension. If they were to contribute £200pcm until the age of 68, rising in line with inflation at 3%, and if that pension generated returns of 5.75% per annum, they’d have a fund of £741,337 on which to retire.

Be aware of changes to the pension rules

As well as annual, carry forward and lifetime allowances controlling how much you can put into your pension tax-efficiently, in 2015, legislation was introduced that provides people with greater control over how they spend, save or invest their pensions. Whilst these reforms are more relevant if you’re about to retire, you should be aware of your options when you start planning your retirement as they might influence how you structure your pension plans. They included enabling people to access their pension from 55, removing the requirement to buy an annuity to generate a guaranteed income until death, and providing access to income drawdown schemes that were previously only available to wealthier pensioners. Read our article ‘Tip pension tips if you’re about to retire’ which provides more details.

Income drawdown enables people to remain invested in retirement while offering them the opportunity to take money from their pension as and when they need it. With annuity rates in freefall since the UK’s vote to leave the EU, it could be argued that income drawdown has never been so attractive to retirees. For example, a 65-year-old with a pension of £100,000 could receive an income of around £5,339 per annum*.

*On a single life, level-rate, no-guarantee annuity.

Alongside the new freedoms, the 2015 legislation introduced a change in the tax treatment of deceased individuals’ pensions. Beneficiaries will now either pay tax at their own income tax level – with the money they receive added to their earnings to calculate this – or, if the person who dies is under 75, there will be no tax to pay. This means that leaving some of your pension to your estate may be a tax-efficient way to plan your legacy.

What can I do if I don’t have enough money for retirement?

Part of the answer could come from planning to work for longer. If you factor in some part-time income for a few extra years, you can supplement your savings and pension, helping them go further – and you may even be able to build extra savings too.

These calculations are not straightforward and, of course, you will need to make assumptions about how much you can expect to earn on your savings and investments which a financial planner may be able to help you with.

Our top tips for starting retirement planning

- Start early – average life expectancy in the UK is getting higher, making retirements longer, so we need more money for later life

- Take responsibility for your own financial future – final salary pension schemes are far less common than they were so the burden is falling on ourselves and not our employers

- Save what you can – a little regular saving now goes a long way in the future

- Regularly check that your plans are still on track – if your circumstances change you may need to adjust your retirement options

- Seek advice when you need it – financial planning can be complicated, especially further down the line when you may have multiple pension pots or more complex requirements. Free pensions advice is available from Pension Wise, or a financial planner can look at your individual situation to ensure all your investments are working in line with your long-term needs.

If you’d like to talk about your future with a Canaccord Genuity Wealth Management specialist in pensions and retirement planning, just call us on +44 20 7523 4500 or email wealthmanager@canaccord.com.

Want to review your retirement planning?

Arrange a no-obligation, complimentary consultation with an independent wealth planner now.

Read more articles here:

- Boost your pension by making use of unused pension allowance

- Am I putting too much into my lifetime pension?

- Top pension tips if you're about to retire

- Post-COVID-19 wealth planning guides

Investment involves risk. The value of investments and the income from them can go down as well as up and you may not get back the amount originally invested.

The information provided is not to be treated as specific advice. It has no regard for the specific investment objectives, financial situation or needs of any specific person or entity.

The tax benefits depend upon the investor’s individual circumstances and clients should discuss their financial arrangements with own tax adviser before investing. The levels and bases of taxation may be subject to change in the future.

[1] Survey conducted by YouGov on behalf of Canaccord Genuity Wealth Management. Total sample size was 2011 adults, of which 1,091 were workers aged 18-64 and 265 have £100k+ of investable assets. Fieldwork was undertaken between 10 – 11 Aug 2016. The survey was carried out online. The figures have been weighted and are representative of all GB adults (aged 18+).

Find this information useful? Share it with others...

Marcus Potter

Marcus works closely with the wealth planning team at Canaccord Genuity Wealth Management. He conducts in-depth research into providing bespoke wealth planning and portfolio management for high net worth individuals.

+44 20 7523 4904

- Wealth news and insights

- Inheritance

- Investing

- Latest market updates

- News & Events

- Retirement & pensions

- Wealth/financial planning

Make the most of your retirement

Investment involves risk and you may not get back what you invest. It’s not suitable for everyone.

Investment involves risk and is not suitable for everyone.