Adding to Positions in Real Estate (REITs)

March 12, 2024

By Tony Brennan, Chief Investment Strategist

The confidence that a soft landing can be achieved for economies and that interest rates will soon be lowered has driven not just the rally in equity markets over the past few months, but also the performance within equity markets. We share the greater optimism about the outlook, but are wary of high valuations and, given risks, can see the possibility of some reversal of recent moves. Consequently, we have added exposure to REITs in our recommended large cap portfolio, with their valuations looking less stretched, but are reluctant at the moment to rotate the portfolio more in a pro-cyclical direction, envisaging the potential for better opportunities in the months ahead.

Sharp Moves Transpiring

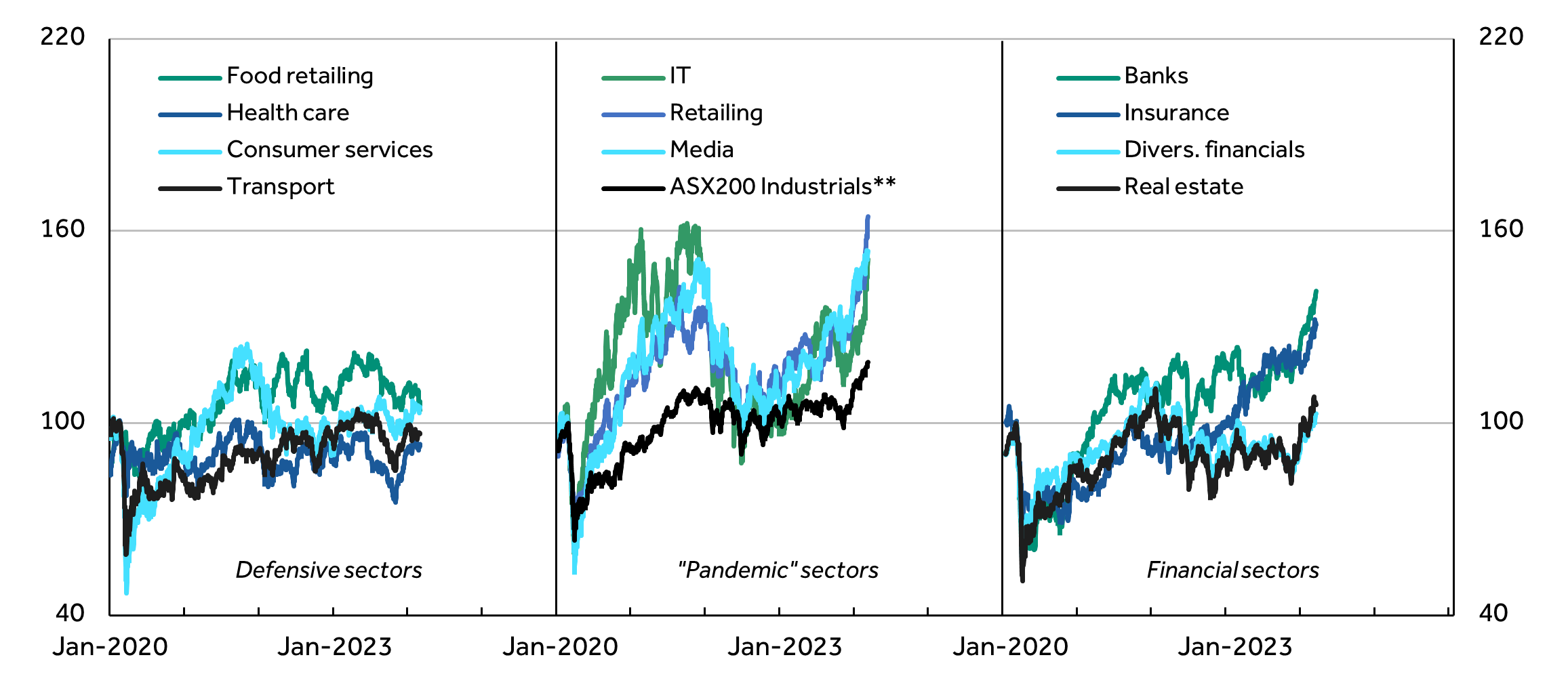

The shift in investor sentiment over the past few months has been stark, perhaps not surprisingly given that “soft landings” after surges in inflation and sharp increases in interest rates have been rare, but look a possibility this time around. With the prospect applying in the domestic economy as well as abroad, the performance in the Australian share market has also reflected it, in the rapid rallies in the more cyclical, interest rate sensitive sectors, which have left more defensive sectors further behind over the past 12 months (Figure 1).

Figure 1: ASX200 sector performance, year to date*

Source: Refinitiv, Canaccord Genuity

*Total return indices. **ASX200 Industrials comprise the market excluding the resources sectors

The IT, media, retailing, and financial sectors have all outperformed strongly in recent months, with only the healthcare sector posting comparable performance among the more defensive sectors. Of course, the pattern of the past 12 months follows broadly its opposite the year before, in 2022, when the rise in interest rates triggered sharp sell-offs in the IT, media and retailing sectors, and resilience in more defensive sectors. But the recovery since has brought the more cyclical sectors back to around their highs in the pandemic, reached in 2021, and also lifted the bank and insurance sectors, while leaving the more defensive sectors and the REITs recording little overall gain from before the pandemic.

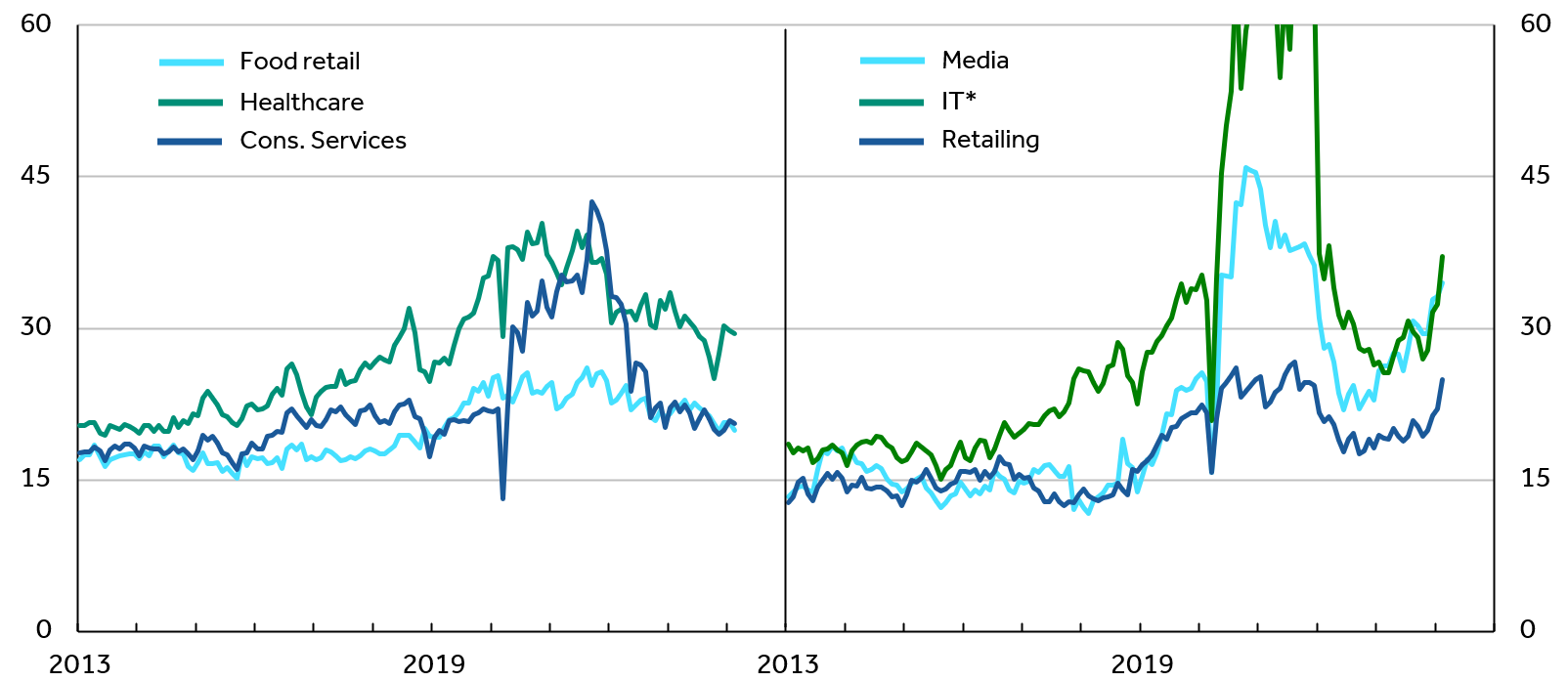

Though these moves reflect investor sentiment about future earnings, they have run ahead of earnings forecasts, and hence have been reflected in relative valuations, for example, in the moves in price earnings ratios (Figures 2). In broad terms, the PE ratios for the IT, media and retailing sectors have risen sharply, and are back above pre-pandemic levels, while those for the more defensive sectors, including healthcare and food retailing, are below levels immediately preceding the pandemic. Across the financial sectors, which tend to have lower PE ratios because of risk, the PE ratio for the banks is high compared to the past decade, but is more moderate for the REITs and is low for insurance.

Figure 2: ASX200 sector price-earnings ratios (selected sectors)

Source: IBES, Refinitiv, Canaccord Genuity

*IT sector PE ratio is truncated for 2020-2021, being elevated partly due to weak earnings

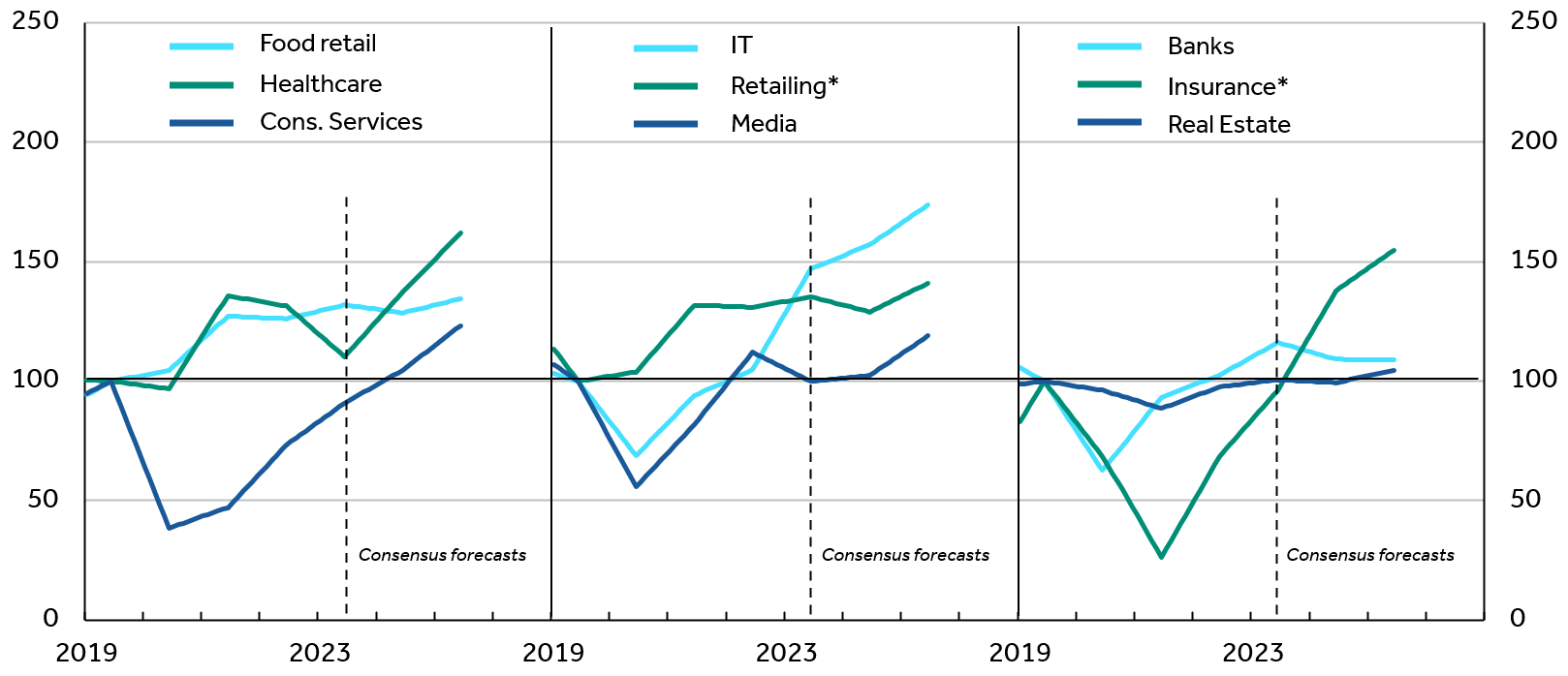

Earnings forecasts, in turn, provide some further perspective on the valuations (Figure 3). For the IT sector, reasonable growth is projected over the next two years, but for media and retailing, little growth is envisaged, no doubt because of the slowdown in the economy. Similarly, for the banks and REITs, growth is also projected to be weak (but the PE ratio for the REITs is more moderate relative to the past). In most of these sectors with subdued growth projected, the outlook would seem likely to need to change significantly to justify valuations, which suggests a potential hurdle to further outperformance. In contrast, for the healthcare and insurance sectors, strong earnings growth is already the consensus view.

Figure 3: ASX200 sector earnings per share (Indexed to FY2019 = 100)

Source: IBES, Refinitiv, Canaccord Genuity

A Bumpy Landing?

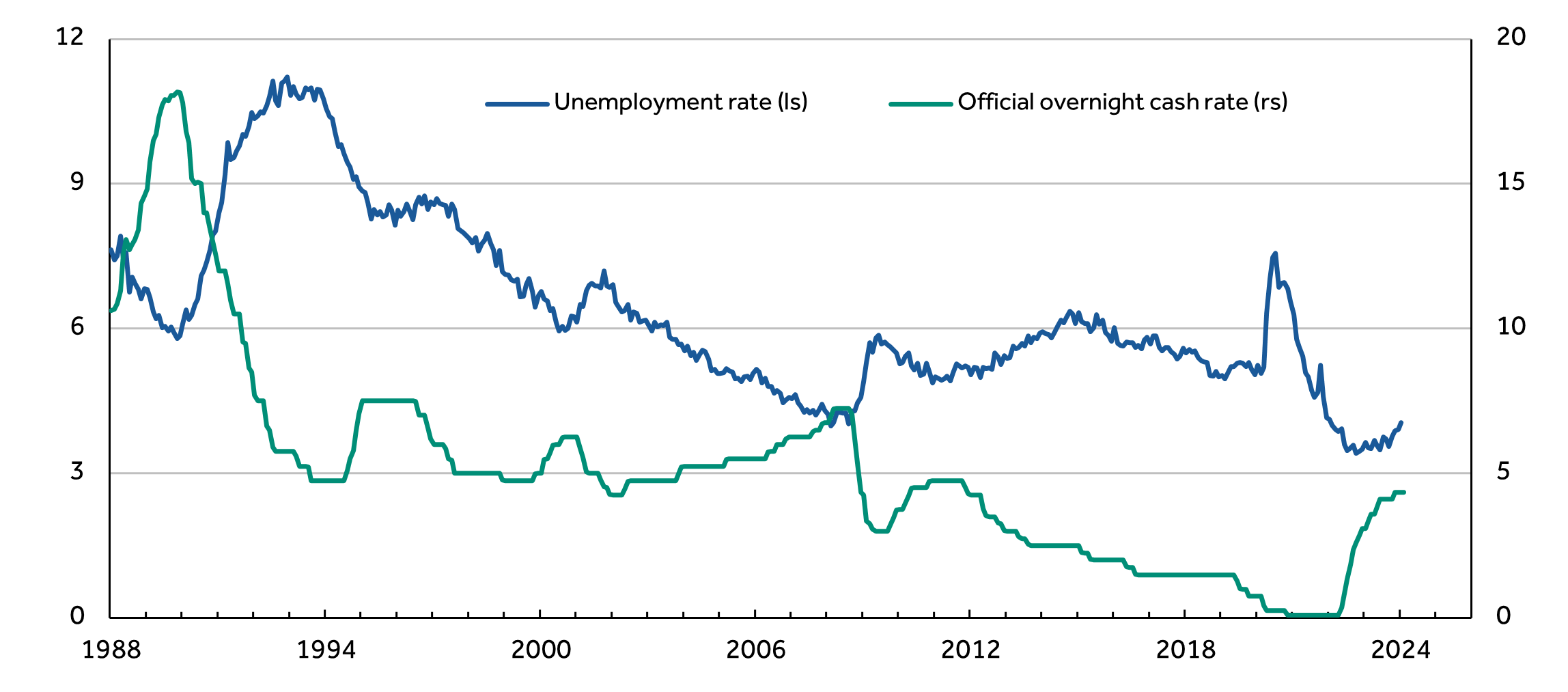

Like others, we consider that the risks to the economic outlook have diminished, though the extent to which markets have reflected this could leave them vulnerable to some retracement. In Australia, like elsewhere, inflation has come down significantly, but still somewhat unevenly, being reflected more in globally traded goods than domestically sourced services, and that of itself could encourage the RBA to delay a lowering of interest rates to ensure more confidence that inflation has moderated sustainably.

On the other hand, the labour market seems to be softening more, with hours worked in particular slowing sharply, and the unemployment rate now looks to be more clearly rising (Figure 4). In fact, further trends in these directions could see the RBA move sooner to a more accommodative policy stance, as it has tended to do in the past in response to rising unemployment – generally cutting interest rates – once it is confident the slowing will reduce inflation sufficiently, and to prevent the economy weakening unduly.

Figure 4: Australia, unemployment rate and interest rates, %

Source: ABS, RBA, Canaccord Genuity

But with lags in the impact of lowering interest rates as much as in raising them, some bumpiness in the economy could be hard to avoid. And with not greatly dissimilar risks in other economies as well, there seems the scope for some retracement in markets, particularly in view of the sanguine outlook that seems to have been priced in. Across the Australian share market, this has encouraged us for the time being to remain overweight some of the defensive sectors – namely healthcare and food retailing – while adding an overweight position in REITs to an existing overweight position in the insurance sector; but remaining underweight IT, communications and the banks in the near term.

Banks and Resources

For the banks, the weak growth outlook reflects the subdued demand for credit, which in turn is contributing to strong competition in mortgage lending and deposit funding, and weighing on margins and core earnings. Lower interest rates could help, but in the near term may be associated with deterioration in loan quality if the economy is bumpy, and higher bad debt charges.

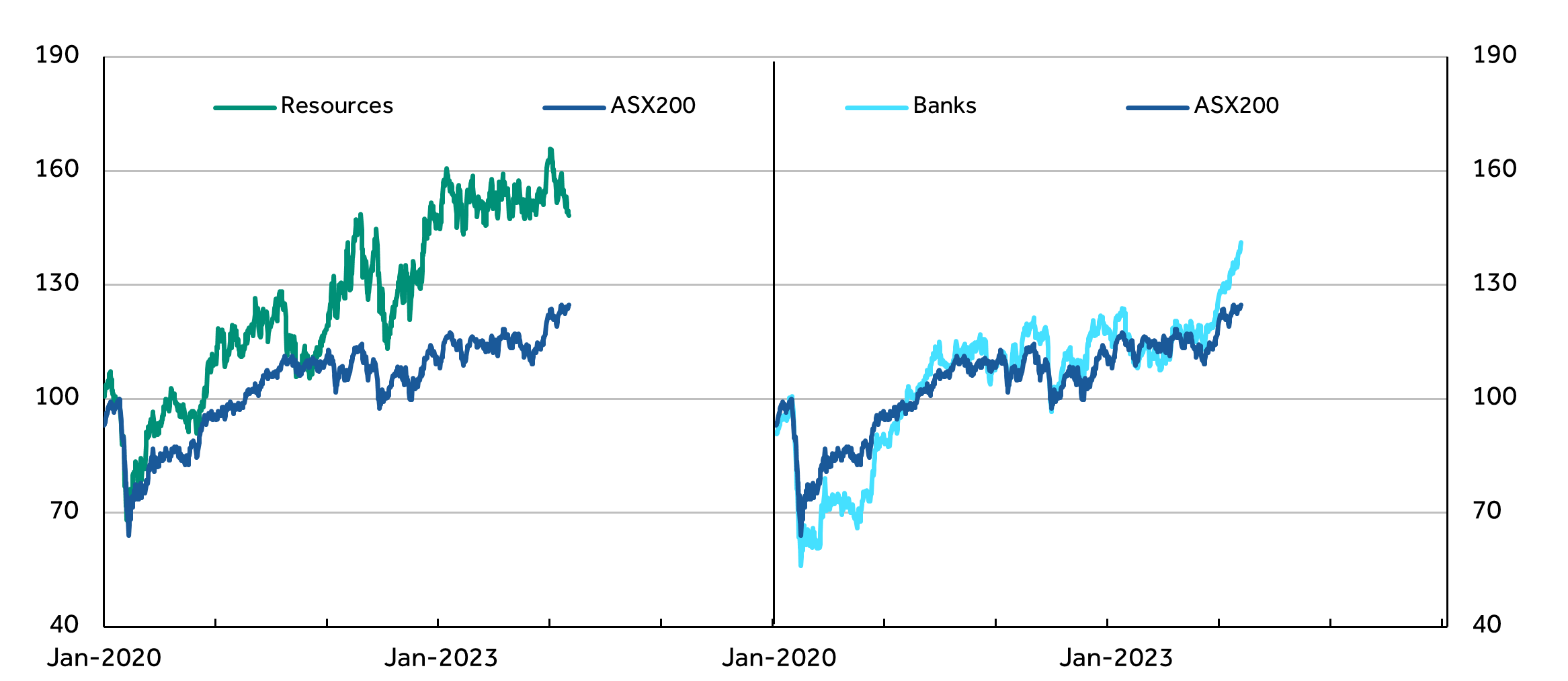

For the resource sector, the other major part of the market, the performance over the years since the onset of the pandemic has been even stronger than for the banks (Figure 5), largely because commodity prices – while they have risen and unwound – have generally averaged higher. In particular, this has been true of iron ore prices (still the most significant for the earnings of the large mining companies in the share market), in turn the consequence of generally higher global steel production, largely driven by China.

Figure 5: ASX200 sector perfomance since the pandemic*

Source: Refinitiv, Canaccord Genuity

*Total return indices.

Though recent steel production figures have been surprisingly weak, there has been some doubt about these; and even were they to be accurate, some bounce-back in production might be expected this year, given China’s desire to sustain GDP growth despite its challenges. With the slump in China’s property sector, and the dampening effect on consumer spending, China may continue to depend on infrastructure and manufacturing investment to support activity and employment and, along with exporting, this could sustain steel production again, hence we remain overweight the resource sector.

Finally, our preference for REITs over other interest rate sensitive sectors at the moment, based on more moderate valuations – not surprisingly after the underperformance of the sector since the pandemic – seems supported by the still relatively low PE ratio of the sector compared to the broader market. However, we have increased weighting through exposure to the industrial, residential, and retail sectors, rather than the seemingly riskier office sector.