Thematic investing – is it the best way forward?

In this article we explore the rise of thematic investing over national or regional investing. In the last twenty years, investment strategies have moved away from specific regions and instead embraced a broader, more thematic approach.

Why might thematic investing present the best way forward?

- It is driven by trends and new developments that are more likely to remain relevant long term

- Many and varied themes encourage diversification, which in turn weathers volatility and fluctuating markets better

- Greater opportunity to tailor your portfolio to what matters to you – often useful for investors who want to prioritise ESG investment themes.

While in the past, a regional focus may have benefitted investors, the same cannot be said today. To invest on a rapidly changing world stage, it is themes rather than nations that point the way forward for investors.

Why investing by region has fallen out of fashion

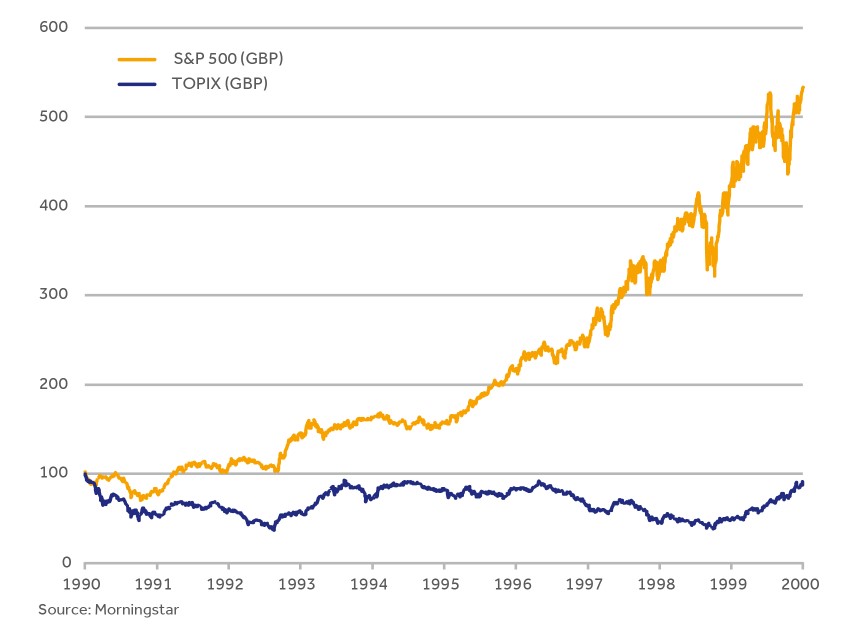

Traditional investment portfolios used to be structured by region or country. If, in the 1990s, you were skilful (lucky?) enough to avoid Japanese equities and concentrate on US equities instead, you would have been very proud of your returns, since Japan fell 16% during the decade whilst the US rose 315%.

The following graph compares the performance of the Tokyo Price Index (TOPIX) with Standard & Poors 500. TOPIX tracks Japan’s largest domestic companies by market capitalisation, while the S&P 500 tracks the performance of the 500 largest US public companies.

Graph of TOPIX vs. S&P during 1990s

Past performance is not a reliable indicator of future performance.

Many investors also liked to 'fly the flag' in their portfolios, favouring their home country, mostly owing to their better knowledge and understanding of domestic companies.

Investment sectors – the search for a star

Both of these trends started unravelling in the 21st century. With the bursting of the dotcom bubble in the early 2000s and the subprime mortgage crisis of 2007-2009, being able to dodge loss-making investment sectors altogether became good for your wealth. Conversely, trying to find the star investment sectors turned into a more profitable quest than figuring out whether the UK market would beat Germany.

This concept was also furthered by the focus on sub-sectors rather than top investment sectors; for instance, cyber-security rather than IT or oncology rather than healthcare. With the arrival of passive investment vehicles (trackers, ETFs) and specialised managers, you could go down to any level of detail. Why invest in the whole energy sector if you really want wind farms?

Investment nationalism was also beginning to take a back seat: if you’re interested in investing in batteries for electric vehicles, do you really care where the companies are headquartered? Indeed, when the COVID-19 vaccines were first unveiled, it was interesting to note that one of the most successful ones was developed by Turkish immigrants in Germany, who then built an alliance with one of the large US pharmaceutical firms. Investment themes were definitely becoming more important than geography.

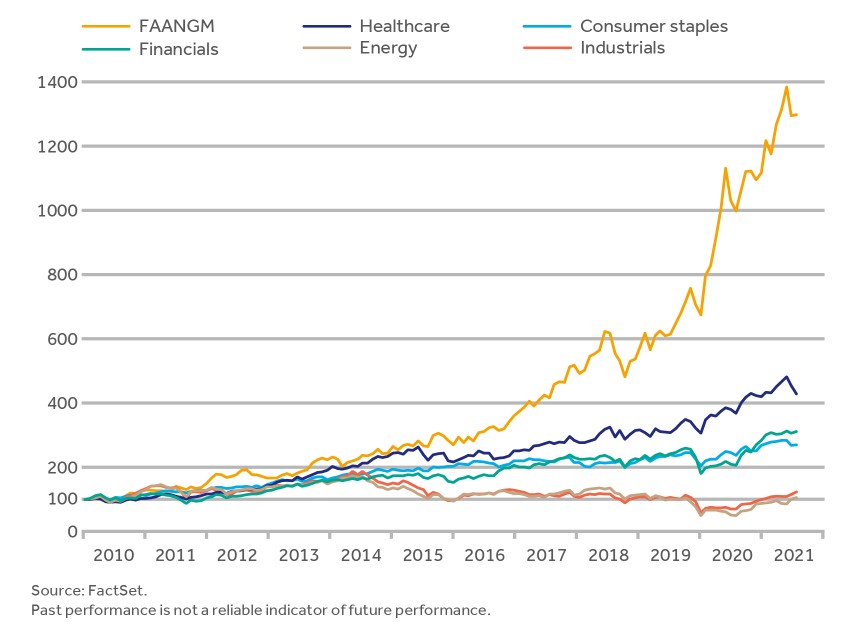

You could point out, though, that over the last 12 years US equities have beaten the rest of the world hands down. If you analyse this more deeply, however, you discover that US equities have benefitted from the booming technology sector, in particular the so-called FAANGM (Facebook, Amazon, Apple, Netflix, Google, Microsoft). Indeed, without these top shares, the US market would not have scored compared to other regions. Ultimately, picking the right sector is crucial.

This is not a recommendation to invest or disinvest in any of the themes or sectors mentioned. They are included for illustrative purposes only.

Returns of FAANGM vs. other US equities

Past performance is not a reliable indicator of future performance.

Investment sectors vs investment themes – what’s the difference?

Investment sectors and sub-sectors are useful as they allow investors to take a diversified and refined approach to building portfolios. They can help mitigate volatility and manage cyclicality as well as allowing us to invest in areas of particular interest or where we have high conviction.

Investment themes can be much broader than sectors, encompassing major trends in society like people living longer, global warming, poorer countries improving their standard of living, etc. In that case, as an investor, we need to figure out which stocks fit the thematic investing trend and will therefore outperform. Broad themes can be turned into smaller ideas, like electric vehicles, vaccines, online shopping, etc. and can therefore be a small part of a larger business area.

Looking at it another way, a portfolio based on sector choices might potentially need to rotate quite a few times during a cycle, as we move from a cyclical recovery to a sustainable expansion, to overheating, to a recession and to a bounce-back. One would have to be very nimble to navigate the sectoral peaks and troughs during these diverse periods.

A thematic investment portfolio, on the other hand, can cover ideas that will remain for 5 or 10 years, through different phases of the economic cycle and should seek long-term outcomes for investors. Will electric vehicles take a bigger share of the car industry over the next 20 years? Will hackers continue to destabilise western countries, creating a need for constantly enhanced cyber protection? As we live longer, will we fall prey to a higher incidence of cancer? Will the US finally bring its infrastructure to the level of other developed countries?

View our developing thematic investment ideas

This is not a recommendation to invest or disinvest in any of the themes or sectors mentioned. They are included for illustrative purposes only.

Beyond investment themes – Focusing on companies

Ultimately, the trick is not just identifying the themes or investment sectors but selecting the individual companies that will benefit from them. Sometimes, an investment theme can outlive its usefulness (once we are all fully equipped with systems to join conference calls, for example) and sometimes a theme can morph into something else (e.g. globalisation turning into robotics as imports are replaced by automated factories).

At CGWM, our investment managers have been active in exploring global thematic ideas through the various stages of the COVID-19 crisis. In the depths of the pandemic the most defensive investments were online shopping, communications systems and healthcare, while in the post-vaccine period we tactically focused on banks, energy and industrial sectors. We also identified longer-term investment themes, such as cyber-security and the battery value chain which can perform well regardless of the macro-economic backdrop.

When investing on your behalf, we are region agnostic, preferring to analyse global trends and take advantage of global themes and thoroughly researched investment opportunities. Currently more than two-thirds of the investments we manage on behalf of our clients are outside the UK, which reflects the breadth and depth of our investment research and global expertise as we look to build our clients’ wealth with confidence. Ultimately, how we identify and classify investment ideas must evolve and reflect the increasingly complicated and connected world we now live in.

Find this useful? Read more here:

Would you like to know more about thematic investing in 2021?

If you would like to find out more about thematic investing, our specific investment themes and our can-do approach to choosing companies, book a complimentary consultation with a Personal Wealth Manager They will be pleased to discuss our thematic investing ideas.

Speak to one of our investment experts

To discuss your investment needs, book a complimentary, no-obligation consultation.

Investment involves risk. The value of investments and the income from them can go down as well as up and you may not get back the amount originally invested.

Charts are for illustrative purposes only and should not be relied upon for any other reason. Information is correct as at date of publication.

The information contained herein is based on materials and sources deemed to be reliable; however, Canaccord Genuity Wealth Management makes no representation or warranty, either express or implied, to the accuracy, completeness or reliability of this information.

Find this information useful? Share it with others...

Michel Perera

Michel is responsible for the investment process and Chief Investment Office at Canaccord Genuity Wealth Management, with a specific focus on asset allocation and investment selection.

Michel is an experienced investment strategist. Before joining CGWM, he spent 19 years at JP Morgan Private Bank where he was the Chief Investment Strategist (EMEA) responsible for running investment strategy and overseeing tactical asset allocation decisions for discretionary portfolios within the region.

Need more help?

Whatever your needs, we can help by putting you in contact with the best expert to suit you.

Investment involves risk and you may not get back what you invest. It’s not suitable for everyone.

Investment involves risk and is not suitable for everyone.