Post-COVID-19 wealth planning: how will COVID-19 affect women's financial prospects?

At Canaccord Genuity Wealth Management, we want to help make financial autonomy a reality for women – even more so in this post-COVID-19 new normal.

The coronavirus does not discriminate. It doesn't care how much wealth you have.

However, it does affect different parts of our society in different ways, and this includes its long-term impact on men and women. For example, in the US twice as many men as women have died from the virus, while 69% of all COVID-19 deaths across Western Europe have been males.

However, whilst there are differences in terms of health, there are also differences in terms of careers and wealth.

The pandemic has hit women hardest

Research suggests the economic impact of the coronavirus could disproportionately affect women’s careers – and so their longer-term financial wellbeing. COVID-19 has targeted sectors such as the leisure industry, hospitality and travel. These sectors are more inclined to employ women, including at senior management levels, and in many cases it is hard, if not impossible, to work from home.

Women have seen a 0.9% increase in unemployment compared to a 0.7% increase for men. This is unusual, as recessions normally hit certain structural sectors harder, such as manufacturing and builders, which employ more men on average.

International institutions like the United Nations and the World Economic Forum have issued dire warnings recently that the pandemic could set women’s economic progress back 50 years, certainly without a supportive childcare infrastructure.

Women undertake a disproportionate share of childcare and home schooling

During lockdown, an acute inequality has emerged between parents, with mothers putting in four more hours a day than fathers are in caring for children at home, no matter what level their job – including highflyers and top executives. Further, the Institute for Fiscal Studies recently interviewed 3,500 families in the UK and found that on average, women were able to undertake just one hour of uninterrupted work, while their male partner could do three.

The expectation that women will sacrifice their own economic viability to provide care at home is at the centre of women’s predicament. And as became evident during lockdown, it is impossible to balance full-time childcare while doing a full-time job at home. Even as nurseries and schools tentatively reopen, there will be knock-on effects for female workers.

Given that the gender pay gap already exists, this extra childcare responsibility could put women back further, and certainly risks impacting their pension planning.

Why are women lagging behind men in investment and pensions planning?

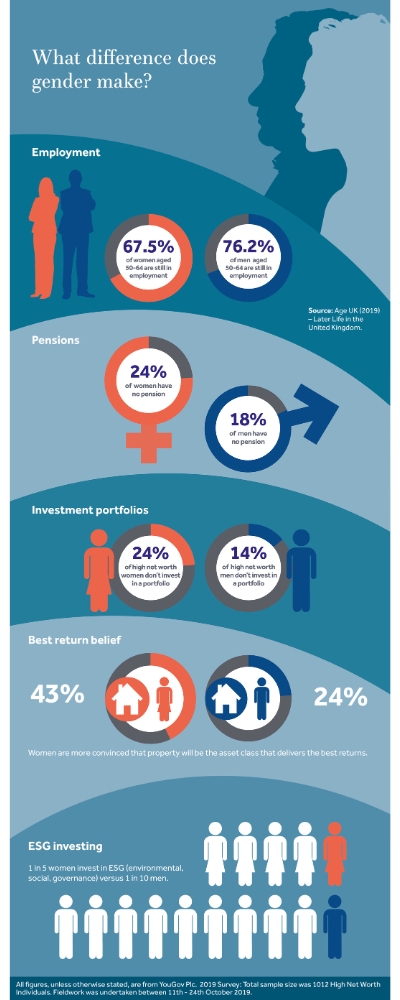

Even when women have savings and wealth, they lag behind men when it comes to investing in the markets. According to our recent survey about a quarter (24%) of high net worth (HNW) women do not have an investment portfolio, compared with 14% of HNW men[i]. Instead, HNW women rely on property investment for their investment needs, and also leave a high proportion of their money as cash savings.

HNW women also have fewer pension investments than men in similar positions. Women fall behind men in pensions saving, partly because of the gender pay gap, but also because they may take time out to bring up children and pause payments into their pension pots in the meantime. However, on average women live longer than men, so it's more important for them to build up pension investments.

According to researchers Kantar, the reasons why women don’t invest are complicated. While the ability to be financially independent is a core aspiration of all women surveyed, the barriers to investment are substantial – including rational and practical reasons but also complex and ingrained emotions. These issues are driving an investment engagement gap, and they found the majority of women have not engaged on the topic of investment in any depth.

At Canaccord Genuity Wealth Management, we find this alarming and want to do more to help. We are genuinely enthusiastic about investing and know the right wealth management plan will not only provide for your financial future but will also instil confidence through financial independence. We want to help make financial autonomy a reality for women – even more so in this post-COVID-19 new normal.

Are women relying too much on property as an investment right now?

Property has served women well for many years. However, as wealth managers, we have always cautioned against putting all one's investment eggs in one basket, and this may be particularly true in a post-COVID-19 world.

In the short term, we have just witnessed the first fall in house prices in the UK since 2012. The one-way bet on property, whilst not as volatile as other investments, is no way guaranteed to keep on rising. This short-term swing is due to the lack of people moving during lockdown – and may be alleviated in part by the Chancellor’s current stamp duty freeze.

However, we can also see COVID-19-induced longer-term trends that might cause property to continue losing value in certain areas. The pandemic may well bring about a shift in the way people work. People are less likely to commute in the same way as before and many may adopt a more local lifestyle. This may shift the high demand for city centre property, particularly highly priced properties in major cities such as London. Furthermore, this societal change could impact demand for commercial real estate, with many firms now reviewing their office capacity.

The risk is that this will disproportionately and detrimentally impact women, especially if they are investing primarily in property and lack a diversified wealth management plan.

Is there any good financial news for women?

The increased flexibility may be one of the silver linings brought about by the pandemic. If we accept that women will continue to shoulder the main burden (and joy) of childcare, the rise of working from home and teleconferencing will benefit them so long as there is also decent childcare infrastructure in place. Zoom has seen an increase of users to 200 million by March this year, from a previous base of 10 million.

More flexibility means more diversity and inclusion in the workplace. This opens up employment to a greater proportion of the potential workforce, including those in later life, disabled people and those who have childcare responsibilities.

This is good for businesses, because diversity promotes creativity and increases capacity for problem solving, while inclusive environments attract and retain talent better than non-inclusive ones. This flexibility will also benefit employers in terms of saved space, fewer fixed office costs (desks, electricity, insurance) and a wider pool of potential talent.

How can wealth planning help women looking at their post-COVID-19 financial future?

We strongly believe investing should be open to all, so we want to give women the confidence they need to make their own investment decisions and become financially independent.

Studies have shown that investing in the markets provides the best returns of any asset class over time, and so our aim is to ensure women (and men) feel comfortable about their investment options and that they can understand the risks associated with the markets. Ultimately, a diverse portfolio of different assets, including a wide range of investments as well as property, provides the best way to secure your financial future.

COVID-19 is bringing marked changes. Maybe you have been affected or can see your own family circumstances, or those of your children, evolving in the future. Planning for these changes or other scenarios has become an imperative and will lead you and your family to make better decisions. Read our blog on how you can use your wealth differently post-COVID-19.

If you feel you would benefit from talking to one of our wealth planning experts about any of these topics, or other issues that are concerning you, please contact us or call us on +44 20 7523 4500.

Let us contact you

If you're unsure which of our teams to contact, let us help you. We can put you in touch with one of our experts who will discuss your wealth management needs with you.

If you would like to read more about wealth planning in the post-COVID-19 world:

- Why diversity and inclusion should matter to investors

- What do I need to know about care homes and care costs?

- Why aren't women investing?

- Should I start saving extra for long-term care at home?

- How can I use my wealth differently in a society being changed by COVID-19?

- How confident does the UK's wealthy feel?

Investment involves risk. The value of investments and the income from them can go down as well as up and you may not get back the amount originally invested.

The tax treatment of all investments depends upon individual circumstances and the levels and basis of taxation may change in the future. Investors should discuss their financial arrangements with their own tax adviser before investing.

Sources:

https://www.theguardian.com/world/2020/jul/07/how-coronavirus-is-widening-the-uk-gender-pay-gap

https://www.bbc.com/future/article/20200409-why-covid-19-is-different-for-men-and-women] [PJ1]

[https://www.bbc.co.uk/news/business-52808930]

Kantar: Winning over Wealth research conducted in Q3, 2018.

[i] All figures, unless otherwise stated, are from YouGov Plc. 2019 Survey: Total sample size was 1012 High Net Worth Individuals. Fieldwork was undertaken between 11th - 24th October 2019. The survey was carried out online.

Find this information useful? Share it with others...

Investment involves risk and you may not get back what you invest. It’s not suitable for everyone.

Investment involves risk and is not suitable for everyone.